How Robinhood's Venture Fund Works - And Why It Changes Investing

May 2026

For decades, ordinary investors largely invested in public companies after they became successful.

The biggest wealth creation often happened much earlier in private markets.

Companies like OpenAI, Stripe, SpaceX, Databricks, and Anthropic reached enormous valuations before most retail investors ever had access to them.

Traditionally, access to these companies was reserved for:

Venture capital firms

Institutional investors

Sovereign wealth funds

Ultra-high-net-worth individuals

Robinhood is now attempting to change that model.

What Robinhood Is Actually Doing

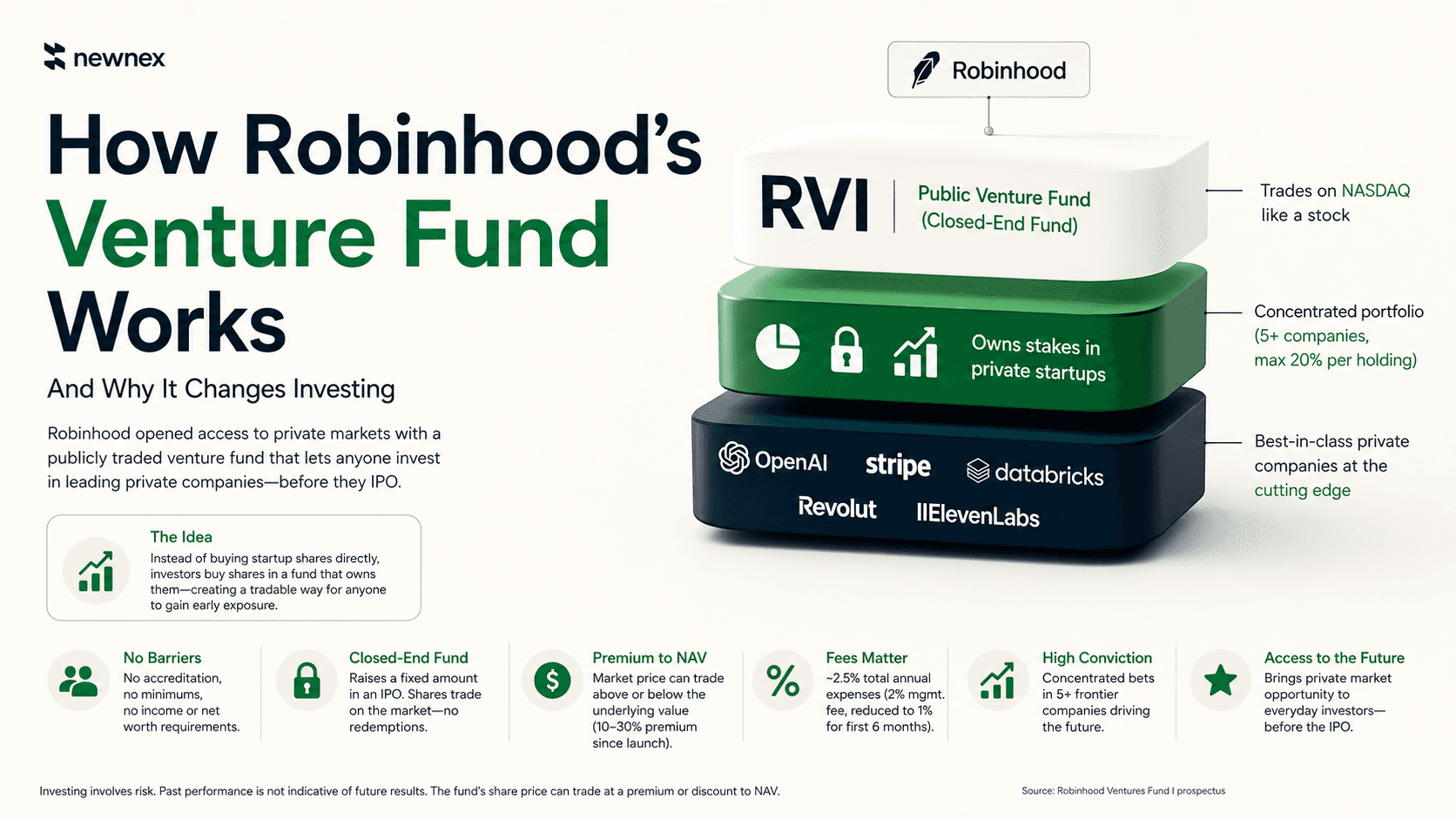

Robinhood created a publicly traded venture investment vehicle called Robinhood Ventures Fund I, ticker: RVI.

Instead of investors buying startup shares directly, they buy shares in a fund that itself owns stakes in private startups.

The structure works like this:

Retail Investors → Public Venture Fund → Private Startup Shares

This means the fund becomes a tradable public asset even though the underlying startups remain private.

In simple terms, people are not buying OpenAI directly. They are buying exposure to a fund that owns OpenAI shares.

Crucially, RVI requires no accreditation, no minimum investment, and no income or net worth thresholds. This is a meaningful shift — previously, investing in private companies typically required being a certified accredited investor, which excluded the vast majority of retail investors.

The fund's IPO raised $314 million.

What The Fund Actually Holds

RVI is not a broad basket of dozens of startups.

It is a concentrated fund, designed to hold stakes in a small number of high-conviction private companies — generally five or more, with no single position exceeding 20% of assets at the time of purchase.

Robinhood calls these "Frontier Companies" — defined as private businesses that are best-in-class and operating at the cutting edge of their sector.

This concentration means the fund's performance is closely tied to a handful of individual bets, not a diversified portfolio.

Closed-End, Not An ETF

RVI is specifically a closed-end fund (CEF) listed on NASDAQ. This distinction matters and is often misunderstood.

A closed-end fund raises a fixed amount of capital through an IPO, creating a set number of shares that then trade on a stock exchange like a stock. Unlike open-end funds, investors cannot redeem shares directly from the fund — they must sell to another buyer on the market.

This is structurally different from an ETF. ETFs have a built-in arbitrage mechanism that keeps the market price close to the value of the underlying assets. Closed-end funds have no such mechanism, which is why the price can drift significantly above or below the true portfolio value.

Why The Fund Trades Separately From Its Assets

Because RVI is a closed-end fund, its share price is set entirely by market supply and demand — not by the value of what it holds.

The underlying startup portfolio has a calculated value called Net Asset Value (NAV), but the market price of the fund can move well above or below this figure depending on investor sentiment.

Since launch, RVI has persistently traded at a premium to NAV of roughly 10–30%, driven by retail enthusiasm and the scarcity of legitimate access to these companies.

The opposite can also happen. Historically, closed-end funds have frequently traded at a discount to NAV. If sentiment cools or private market conditions weaken, the share price could fall toward or below the underlying portfolio value - a classic CEF risk that investors should understand before buying.

The Real Cost Of Access

The document often discussed here omits something important: fees.

RVI charges approximately 2.5% in total annual expenses. The management fee alone is 2% per year of net assets, reduced to 1% for the first six months following the IPO. There is no performance fee or carried interest.

These fees are deducted from the fund's assets, which means they are paid indirectly by shareholders and gradually reduce NAV over time.

Combined with a 10–30% premium to NAV at the time of purchase, the effective cost of access is meaningful. For non-accredited retail investors with no other route into these companies, many consider that premium worth paying. For accredited investors who can access private secondaries directly, it is a harder case to make.

Why Investors Are Interested

Retail investors increasingly feel locked out of modern wealth creation.

The number of publicly listed companies in the US has fallen from around 7,000 in 2000 to roughly 4,000 today, while private companies are growing in both number and estimated value — now surpassing $10 trillion in the US alone.

Many major technology companies now stay private much longer than before. By the time a company reaches public markets:

Much of the explosive growth may already have happened

Early investors may already have made enormous returns

Valuations may already be very high

This creates demand for earlier exposure.

The rise of AI amplified this dramatically. Many investors now believe:

A few AI companies could become trillion-dollar businesses

AI infrastructure may reshape entire industries

Missing early AI opportunities could resemble missing early internet or smartphone companies

As a result, vehicles offering exposure to private AI startups can attract intense demand.

Why The Price Can Rise Far Above The Assets

One important concept is that closed-end funds do not always trade at the value of the assets they hold.

The market price may rise above the underlying portfolio value because investors are paying for:

Access

Scarcity

AI exposure

Future expectations

Narrative momentum

In other words, people may value the possibility of future upside more than the current accounting value of the assets.

This creates what financial markets call a "premium to NAV."

But the reverse is equally possible and historically more common. If the narrative fades, if portfolio companies disappoint, or if broader market conditions shift, the fund can trade at a significant discount to NAV — meaning investors could lose money even if the underlying companies hold their value.

Why This Model Is Powerful

Robinhood is effectively transforming venture capital into a consumer financial product.

Historically, venture investing was:

Illiquid

Long-term

Exclusive

Difficult to access

Robinhood is trying to make it:

Tradable

App-native

Retail-accessible

Narrative-driven

This is a major shift in how private capital markets may evolve.

The Bigger Financial Shift

Modern investing is increasingly moving toward exposure-based finance.

People are not only investing in current profits or factories anymore. They are investing in:

Themes

Narratives

Future possibilities

Technological transformation

Access to future ecosystems

AI intensified this trend because it created enormous expectations around future economic value.

As a result, the financial value of "access to the future" itself is becoming tradable.

That is the deeper reason why Robinhood's venture fund model works - and why understanding its structure, costs, and risks matters just as much as understanding its appeal.

NEWNEX - a private network where VCs share deals with other VCs for syndication and co-investment, while LPs collaborate with other LPs on opportunities and manage GP relationships in one place.

Built for direct, trusted connections by default - private-first, with no SPVs, no intermediaries, and no unnecessary layers between investors. www.newnex.io