26 March 2026

The venture capital market is undergoing a structural shift. What was once a broad, rising tide lifting many startups is now splitting into a K-shaped dynamic - where a small group of companies accelerates rapidly with abundant capital, while the majority face slower growth, constrained funding, or stagnation.

This is not a short-term cycle. It is a reflection of a deeper change in how capital is allocated, how companies scale, and how venture returns are generated.

Recent reporting from TechCrunch, including developments involving firms like Andreessen Horowitz, highlights a clear pattern: capital is moving faster, in larger amounts, into a narrower set of high-conviction opportunities.

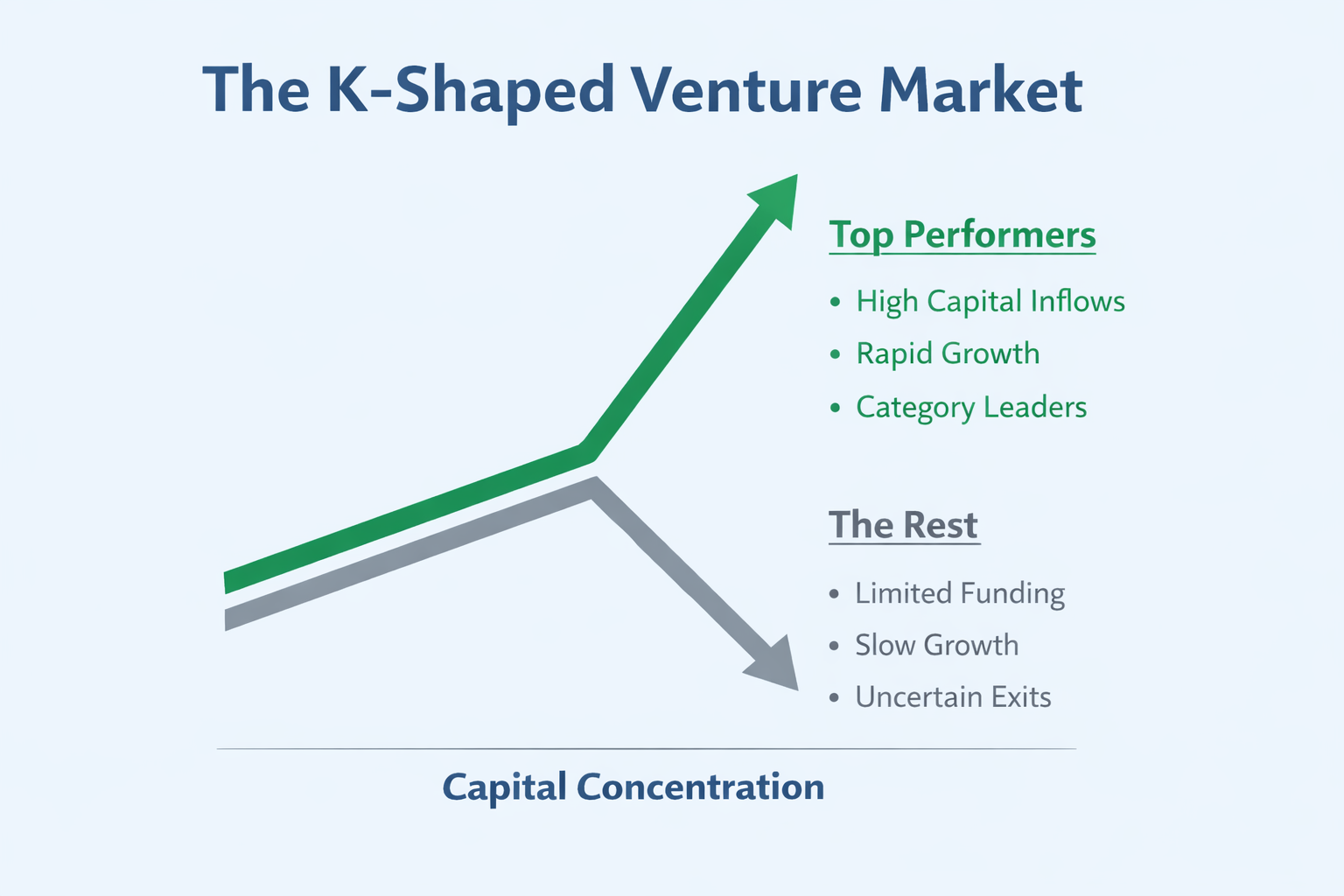

What “K-Shaped” Means in Venture

At the top of the “K”:

- A small number of companies attract disproportionate capital

- They scale rapidly, often driven by AI, infrastructure, or strong network effects

- They secure top-tier investors and follow-on rounds quickly

At the bottom:

- A large number of startups struggle to raise subsequent funding

- Growth is more linear or constrained

- Exit visibility becomes uncertain

This is no longer just about performance - it is about access to capital becoming unevenly distributed.

Why Capital Is Concentrating

1. Winner-Takes-Most Markets

Technology - particularly AI - is amplifying scale advantages. Early leaders can dominate quickly, making them natural magnets for capital.

2. Speed Has Become Critical

The best companies scale globally in months. Investors are concentrating capital to accelerate speed and secure market leadership.

3. Larger Funds, Fewer Bets

Many leading venture firms are writing bigger cheques into fewer companies, prioritising conviction over coverage.

4. Signalling Effects

When a top-tier firm invests, it often validates the opportunity for others — further concentrating capital into the same companies.

The Expanding Gap Between “Good” and “Great”

Venture capital has always relied on outliers. But today, the gap between:

- Category-defining companies, and

- Everything else

…is widening.

Strong, well-run businesses may still exist in large numbers. But without the potential for breakout scale, they are increasingly less aligned with traditional venture return models.

Should VCs Still Invest Broadly?

Rather than a binary yes or no, this is increasingly becoming an open strategic question across the industry.

In a K-shaped market, where outcomes are more concentrated, funds are rethinking how broadly they should deploy capital — and what truly drives performance.

In practice, many VCs continue to invest across a wide range of companies. This is shaped by several realities:

- The need to deploy committed capital within a defined timeframe

- Limited access to highly competitive, oversubscribed deals

- A belief that differentiated insight can uncover overlooked opportunities

At the same time, the market is raising important considerations:

- Not all companies attract strong follow-on capital

- Growth trajectories are diverging more sharply

- The gap between solid businesses and venture-scale outcomes is increasing

This is prompting a broader reflection within the industry:

- Should portfolios remain diversified to maximise exposure?

- Or become more concentrated to align with where outsized returns are emerging?

The answer is becoming less about “right vs wrong” — and more about strategy, access, and conviction.

Some funds are leaning into concentration, backing fewer companies with higher conviction. Others continue to invest broadly, particularly where they believe they have a unique sourcing or underwriting edge.

What is becoming more difficult to sustain is the middle ground — investing broadly without a clear differentiating advantage.

What Winning VCs Are Doing

The most effective investors in this environment are adapting in a few consistent ways:

- Focusing on high-conviction investments rather than wide coverage

- Reserving more capital for follow-on rounds in their strongest companies

- Moving quickly to secure allocation in competitive deals

- Avoiding “middle-zone” companies that are solid but unlikely to deliver outsized returns

The shift is clear: from diversification toward precision and conviction.

Implications for Founders

For founders, this environment raises the bar significantly.

Raising capital is no longer about being “good enough.” Increasingly, investors are looking for:

- Clear potential for category leadership

- Strong early traction or differentiation

- Speed of execution and scalability

- The ability to attract follow-on capital

Companies that cannot demonstrate these may still build meaningful businesses — but may find it harder to align with venture funding expectations.

What To Do About It

1. Prioritise Access

The key advantage in today’s market is not volume of deals — but access to the right deals.

2. Build Clear Investment Thesis

Generalist approaches are becoming less effective. Strong, focused theses help identify true outliers earlier.

3. Increase Selectivity

Doing fewer deals with higher conviction is becoming a more common strategy among top-performing funds.

4. Double Down on Winners

Reserving capital and supporting breakout companies is critical to capturing full upside.

5. Strengthen Networks and Syndication

Access is often driven by relationships. Collaborative investing and trusted networks are becoming more important.

6. Recognise Different Paths

Not every strong company fits the venture model. Distinguishing between venture-scale and non-venture-scale opportunities is increasingly important.

The Strategic Shift Ahead

The K-shaped venture market is not a temporary distortion — it reflects a more fundamental evolution:

- Fewer companies will capture a larger share of value

- Capital will continue to concentrate around perceived winners

- Access and conviction will define performance

For investors, the central question is no longer how to see more deals — but:

How to consistently identify and access the few companies that will define the future.

Those who adapt to this shift will continue to outperform.

Those who do not may find themselves active in the market — but increasingly on the wrong side of the curve.

----

Newnex enables direct access between VCs - privately, without intermediaries.

Join 50+ venture capital firms already connecting with each other for high-quality deal flow in a trusted environment.

0

Comments